Benji Financial

Canada’s first neobank for small businesses

Benji Financial was a free business operating account that combined deposits, bookkeeping and spend management—all in one place. Unlike a traditional bank where users have limited access to core banking functionality based on the plan selected, Benji Financial made it easier and more affordable for small business owners to manage their finances in one place. On average, users could open a business operating account in less than 10 minutes. With the account, users could easily use their Benji Financial card to pay for business expenses, have all their transactions auto-categorized, and even open sub-accounts to help manage their funds (e.g. taxes, vacation, equipment, etc.).

We successfully launched Benji Financial in January 2022, and had users signing up from across Canada. Unfortunately, we had to shut down Benji Financial six months after launch when our BaaS provider—who was also our banking partner and one of Canada’s largest banks—decided to end their investment in this service. We had to quickly help our users move their funds to another bank and let go of our employees and subcontractors. It was a painful learning experience that has since changed our approach to building products.

Timeline

May 2021–Jun 2022

Platforms

Disciplines

Tools

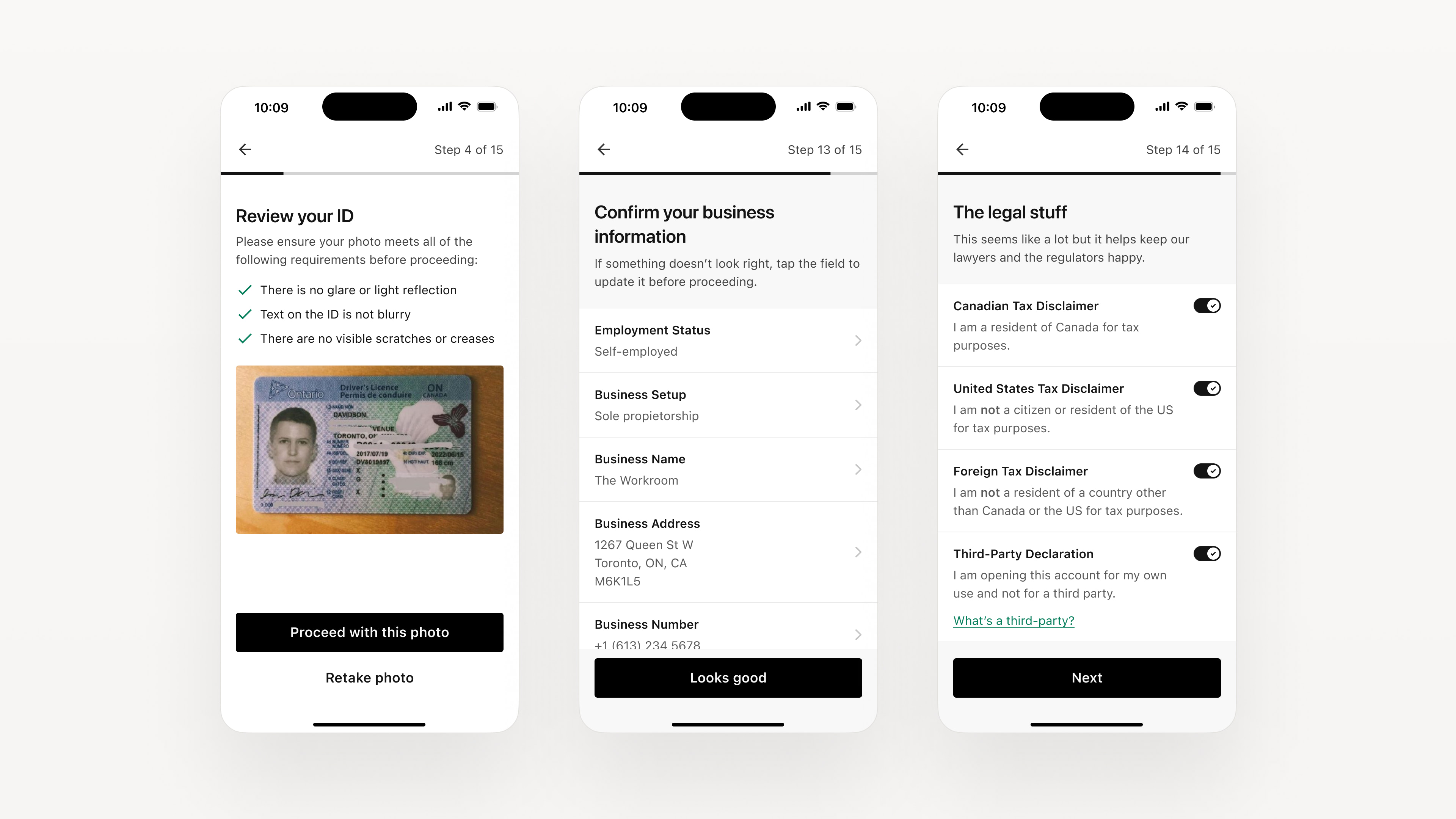

User Onboarding

Banking is a heavily regulated industry in Canada and since our banking-as-a-service (BaaS) provider was also one of Canada's largest banks, we had to meet strict platform requirements in addition to know your client (KYC) and anti–money laundering (AML) compliance. Initially, our BaaS provider wanted us to either ask or have our users accept 108 questions and agreements. This seemed ridiculous to us considering how long it would take users to open a bank account. To meet our internal goal of opening a bank account within 10 minutes, we went through all the questions to see how we can satisfy the requirements without having the process feel overwhelming to the user. We decided to split our onboarding into two parts: 1) sign up and 2) open account.

The sign up flow was shorter with questions about the person. The second flow was longer with questions about the business along with the identity verification process. By having a shorter flow that was about the person, we were able to create an opportunity for a "quick win" and help build momentum for the user. Plus, since most of the questions were about the user, we could take advantage of AutoFill to speed up the sign up flow. For the second flow, we autofilled all fields that required user's info along with some informed assumptions (e.g. for the field "employment status," we can confidently auto-select "self-employed" from the dropdown menu) while giving users the ability to make changes. This approach satisfied all the requirements while ensuring our users could seamlessly open a bank account in 10 minutes from the comfort of wherever they were.

User Activation

Prior to launching our offering, we set up a landing page where people could sign up for early access. Once the person submitted their name and email, we redirected them to a Typeform survey. This survey was intentionally long; about 7–10 minutes to complete. We wanted to see how many people would take that much time to tell us about themselves and their business sole for the opportunity to “move up the line.” Strangely, when we reached out to these “early birds” at our beta launch time, most didn’t respond to our outreach or didn’t followthrough on the second step of the onboarding flow. It was an odd behaviour. When we inquired, we were explained that they had already opened a business bank account with a traditional bank or they weren’t ready yet to open an account with us until we had more specific features.

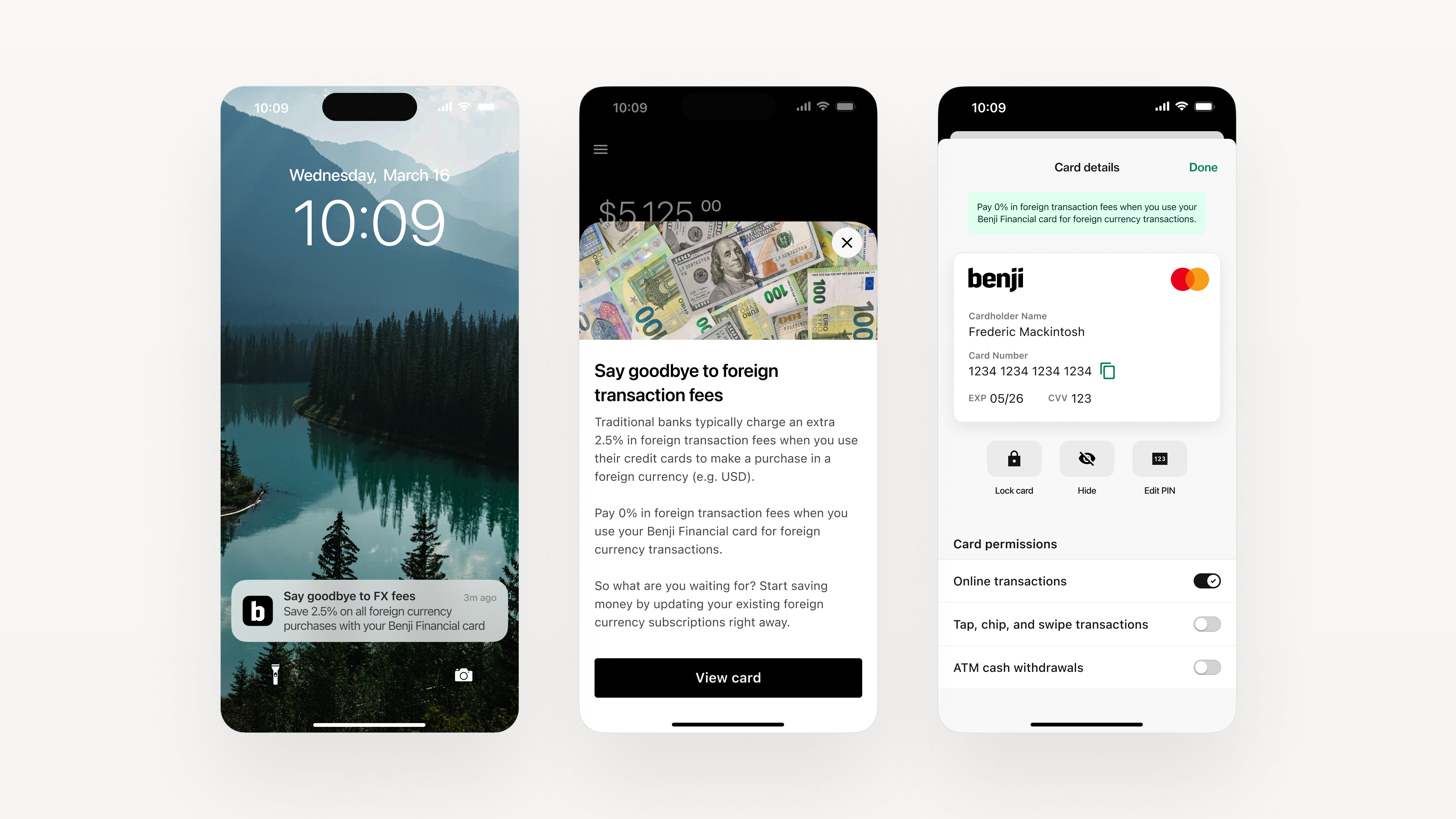

For those who did open an account, we didn’t consistently notice an immediate use of their account. Even those who deposited money didn’t always use their account regularly. It was only when users had setup their Benji Financial card for recurring business expenses that they started using the account more regularly. This insight drove us to focus on getting every user to update an existing subscription with their Benji Financial card. Since Benji Financial was designed for Canadian business owners, we knew that just about everyone had at least one subscription that was charged in USD, if not most. Since we weren’t charging foreign transaction (FX) fees on our card, we highlighted this feature to encourage users to replace their existing cards with their Benji Financial card for subscriptions. This approach quickly helped us gain more active users.

Sub-accounts

Soon into our launch, a number of our users were asking for the ability to open additional accounts. We thought this to be an odd request so we decided to investigate. Turns out users who were asking for an additional account wanted a place to set aside money for taxes and other upcoming purchases. Moving this money into a separate account would ensure they don't end up spending it or paying it out to themselves as distributions. With this in mind, we created "Pockets." These were sub-accounts to help business owners (visually) set aside funds for taxes, vacation, equipment, etc. Users could also choose to set a percentage of all business income to be automatically transferred to a Pocket each time funds were deposited into their business operating account. We also added the option for users to set a fixed amount to be transferred at a specified occurrence. By approaching this as a sub-account, we eliminated the need to go through another account opening process, while still making it easier for users to stay on top of their finances.